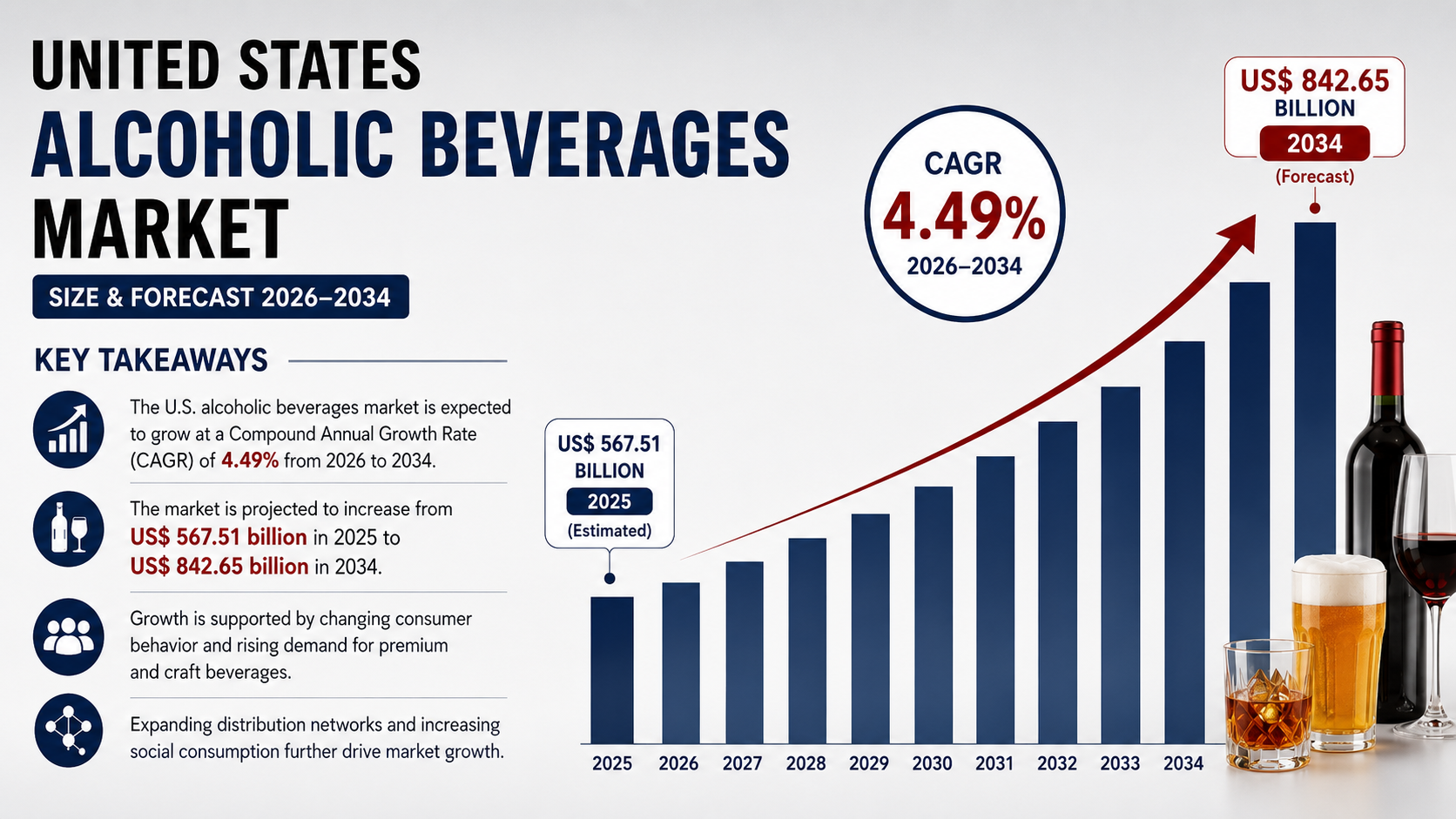

Checking In on Brown Spirits: A Category at the Crossroads

After two decades of almost uninterrupted ascent, the world of whiskey, aged rum, and reposado has hit a genuine reckoning. The numbers tell a story of correction, not collapse, and of a market splitting in two.

For twenty years, brown spirits could do no wrong. Bourbon became a cultural phenomenon, single malt Scotch a luxury asset, and aged agave a status symbol. Distilleries expanded, prices climbed, and the aging warehouses of Kentucky and Speyside filled to bursting. Then, somewhere around 2023, the music slowed. American whiskey volumes fell for the first time since 2002, Scotch posted its first meaningful declines in memory, and by early 2026 the news had turned genuinely sobering.

For nearly two decades, brown spirits appeared unstoppable. Bourbon demand surged, Japanese whisky became nearly impossible to find, premium Scotch expanded globally, and aged rum began attracting serious enthusiasts.

The temptation is to read this as a bust, a bubble finally popping. That reading is too simple. What is actually happening is a correction after years of overheated growth, complicated by a once-in-a-generation drop in how much people drink, by trade wars that severed key export markets, and by a glut of aged stock that producers cannot easily unwind. The category is not dying. It is being forced, sometimes painfully, to rediscover discipline.

The Scoreboard: Who Is Thriving, Who Is Surviving

The headline figures are stark. For the twelve months ending July 2025, total US whiskey sales fell nearly five percent by both volume and revenue, and the story worsened from there. Bourbon, the engine of the boom, slipped around one and a half percent, a modest number that nonetheless masks real distress given how much new production had been banked against endless growth. Kentucky now holds a record sixteen million barrels of aging whiskey against a shrinking market, an oversupply that will take years to work through.

Beneath the topline, the subcategories diverge sharply. Blended Scotch fell hardest, down nearly nine percent in the US, while single malt proved more resilient. Irish whiskey, skewing younger and more exposed to tariffs, dropped more than six percent. Aged tequila, the darling of the previous cycle, has cooled dramatically as consumers trade down from expensive añejo bottles toward cheaper expressions. The clearest bright spot is aged rum, particularly at the super-premium end, where brands like Diplomático and Brugal continue to post growth even as nearly everything around them contracts. Survival, right now, depends almost entirely on where a spirit sits on the price ladder.

The View from the Boardroom

The pressure is written plainly across the industry's biggest names. Brown-Forman, maker of Jack Daniel's, cut roughly twelve percent of its workforce and watched its tequila portfolio decline by double digits as Herradura and el Jimador lost ground. Diageo, the largest player of all, reported tequila down seventeen percent in a recent half-year, dragged by steep declines at Casamigos and Don Julio, and temporarily halted whiskey production at its Balcones and George Dickel distilleries. Edrington, the house behind Macallan, saw annual profits fall twenty-six percent and sold off Famous Grouse to concentrate on ultra-premium bottles.

Yet even here the picture is not uniform gloom, and the nuance matters. Macallan's prestige expressions, the twenty-five and thirty-year-old bottles, sold slowly, but its accessible twelve-year-old core range grew by double digits and actually gained market share. Diageo's rum and Scotch categories eked out organic growth even as its agave spirits cratered. The lesson emerging from the earnings calls is consistent: the ultra-luxury tier that powered the boom is now the most exposed, while dependable core brands at sensible prices are quietly holding the line. Companies with the broadest price architecture are weathering the storm best.

The Forces Underneath

None of this is happening in a vacuum, and three forces are converging at once. The first is the broad decline in drinking itself, with US consumption rates hitting a ninety-year low as younger adults embrace low and no-alcohol options, question alcohol's health effects, and in some cases substitute cannabis. This is the structural shift the industry least anticipated and can least control. When the overall pool of drinkers contracts, even a beloved category cannot simply grow its way out.

The second force is self-inflicted. During the boom, producers ramped output far faster than demand, and retailers pushed prices to levels that everyday bottles never deserved, turning affordable staples into scarce trophies and eventually alienating the very drinkers who built the category. The third is geopolitical. Trade disputes and tariffs have battered exports, with American whiskey pulled from Canadian shelves entirely, a move one executive called worse than tariffs. Distillery pauses, from Jim Beam's flagship Kentucky site to malting facilities in Scotland, are the visible scars of these combined pressures. The correction, in other words, was partly earned, partly imposed, and wholly unavoidable once the momentum broke.

The Takeaway

Brown spirits are not in freefall, whatever the grimmer headlines suggest. They are moving through a long-overdue correction, shedding the speculative excess of a boom that could never have lasted and returning to something closer to fundamentals. The distilleries pausing production and the workforces being trimmed are real hardships, but they are also the mechanism by which a bloated market rights itself. Aging inventories will normalize, and the producers who survive will emerge leaner and better matched to actual demand.

The deeper signal is the bifurcation running through every subcategory and every balance sheet. The market is splitting between an ultra-premium tier now paying the price for its own excess and a value-conscious core that keeps drinkers engaged at fair prices. Aged rum thrives, prestige Scotch stumbles, accessible bottles endure, and the parent companies best positioned are those humble enough to serve the whole ladder rather than only its top rung. For anyone who loves these spirits, the moment is less a funeral than a reset, a reminder that quality and reasonable pricing, not hype and scarcity, are what sustain a category over the long run. The boom is over. The craft, thankfully, is not.

Frequently Asked Questions

What are brown spirits?

Brown spirits generally refer to barrel-aged distilled beverages such as bourbon, rye whiskey, Scotch whisky, Irish whiskey, Tennessee whiskey, aged rum, Cognac, Armagnac, and many reposado and añejo tequilas.

Is the brown spirits category declining?

Not broadly. Growth has slowed after years of exceptional expansion, but most analysts view the current environment as a market correction and normalization rather than a collapse.

Why did whiskey become so popular over the past two decades?

Premiumization, cocktail culture, bourbon tourism, collectible bottles, strong marketing, and growing consumer interest in craftsmanship all contributed to sustained demand.

Are premium spirits still selling well?

Yes. Ultra-premium bottles generally continue to perform better than many mid-priced offerings, reflecting the broader K-shaped economy in which affluent consumers remain willing to spend.

Why are some distilleries slowing production?

Many producers expanded aggressively during the whiskey boom. As inventories have grown and demand has moderated, some distilleries are reducing production to better align future supply with expected market conditions.

What alcohol content do most brown spirits have?

Most standard bottlings are released at 40% to 46% ABV (80 to 92 proof), while bottled-in-bond expressions are 50% ABV (100 proof) and cask-strength releases often exceed 55% ABV.

How long are brown spirits typically aged?

Aging varies widely. Bourbon may range from 2 to 12 years or more, Scotch often matures for 10 to 18 years, while premium rums, Cognacs, and other aged spirits follow their own maturation requirements depending on regional regulations.

What does the future look like for brown spirits?

The category is likely entering a period of slower, more sustainable growth. Producers that emphasize authenticity, hospitality, transparency, and compelling consumer experiences are likely to outperform those relying solely on premium pricing.